Fixed rate mortgage holders exiting five-year fixed rate deals are being urged to check their mortgage contracts closely as many may be entitled to a tracker mortgage with their lender.

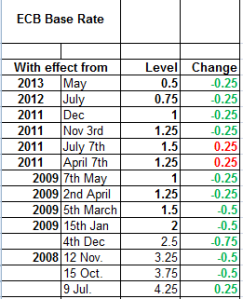

Throughout the summer of 2008, many mortgage customers began opting to fix the rate of interest on their loans in response to rising interest rates by the European Central Bank. By the summer of 2008, the European Central Bank had increased the base rate of interest to 4.25% resulting in a majority of tracker mortgage holders paying in excess of 5% on their loans.

Many borrowers began choosing the security of a fixed rate as protection against rising interest rates.

“While it is extraordinary to imagine now, tracker mortgages were fast falling out of favour with borrowers during the late spring and summer of 2008″ said Mr Frank Conway, founder of the Irish Financial Review.

“A lot of people were opting for fixed rate loans as protection against rising interest rates, which were expected to continue rising as the ECB battled inflation” said Mr Conway.

Within months of locking into their fixed rate mortgages, the European Central Bank began its extraordinary cycle of interest rate cuts.

It is estimated that between 5,000 and 10,000 mortgage holders will exit five-year contracts during 2013. A high proportion are expected to revert to tracker arrangements as a condition of their loan, particularly those that closed before October 2008.

On a €250,000 mortgage, moving from a 5-year fixed rate deal costing 4.95% to a tracker deal of 1.5% (1% over ECB) customers will see their monthly repayments falling from €1334.42 to €862.80, a savings of €471.62 per month based on calculations provided by Mr Conway.

“Understanding the detail of one’s mortgage is always extremely important. One couple that recently discovered that they were entitled a tracker deal only discovered their luck when informed by their bank,” said Mr Conway.

Tracker mortgages ceased being offered by banks by mid-November 2008 following the height of the credit crunch.