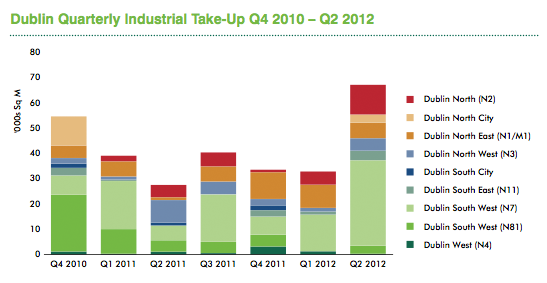

There was a surge of industrial transactions completed in Dublin during Q2 2012, with take-up in the three month period more than double that achieved in the first quarter of the year. More than 67,000 square metres of industrial accommodation was let or sold in Dublin over the last three months, representing an increase of over 100% on the volume of activity in this sector quarter-on-quarter and over 140% on transaction volumes in the same quarter in 2011. Leasing activity dominated, accounting for more than 80% of industrial take-up in Q2 2012.

One particularly large transaction, a letting at Kilcarbery Business Park in Dublin South West (N7), somewhat exaggerates the take-up figures for the quarter however. Although full details of the letting remain confidential, this transaction (the largest industrial letting to sign in the capital since the end of 2009) accounted for over 22,000 square metres of the total 57,000 square metres leased in Dublin in the last three month period. However, encouragingly, even without this transaction, the level of leasing take-up achieved in Dublin in Q2 2012 was still stronger on both a quarterly and annual basis.

The Dublin South West (N7) corridor accounted for over 55% of Q2 industrial take-up although this result is somewhat skewed by the large letting in Kilcarbery. The Dublin North (N2) corridor accounted for a further 17% of the total quantum of industrial accommodation leased in Q2.

Of particular note this quarter is the number of large leasing transactions which were signed throughout Dublin. 14 out of the 31 industrial letting transactions signed in Q2 were over 1,000m2 in size, while 73% of the accommodation leased was in units extending to more than 2,000m2 in size.

Recent analysis carried out by CBRE showed that there has been a doubling in the number of global retailers that can deliver goods purchased online to Irish consumers since the beginning of 2011, making Ireland the fifth most developed online market globally. This trend is having an impact on the industrial sector with logistic and distribution occupiers particularly active over the last quarter. Although details remain confidential, the large letting in Kilcarbery is thought to have been signed by a food distributor, while Fastway Couriers let 4,845 square metres at Crosslands Industrial Estate in Dublin South West (N7) and furniture retailer DFS leased a unit in Rosemount Business Park in Dublin 15 to facilitate distribution to their recently opened store at Blanchardstown.

Dublin continues to evolve as a data centre hub for cloud computing and modern data storage. This has fuelled demand from the ICT sector in recent months. However, corporate budgetary considerations are heavily influenced by the ongoing crisis in the Eurozone, which will have implications for demand in this particular sector of the industrial market for the foreseeable future.

Demand for industrial accommodation increased during Q2 2012, with our register of active requirements showing demand for more than 100,000 square metres of accommodation at the end of the quarter – a 40% increase in requirements from last quarter. While demand for industrial accommodation is not focused on any one location of the city, occupiers have become more specific in terms of the size and quality of accommodation they require. Large industrial units continue to be sought after by potential occupiers, with over 70% of registered requirements focused on units that extend to more than 1,858 square metres (20,000 sq ft) in size. More than a quarter of demand at end of Q2 2012 was specifically focused on units of more than 4,645m2 (50,000 sq ft) in size.

Having contracted slightly at the start of 2012, prime rents for industrial accommodation in Dublin now appear to have stabilised at approximately €60 per square metre. As the supply of prime facilities continues to contract and with no speculative development in the pipeline, prime rents should remain at this level despite wider economic pressures. An increase in the availability of secondary industrial properties, many of which have been brought to the market by receivers and banks in recent months, continued to put further pressure on rents for non-prime buildings in the capital during Q2.

There were no large industrial investment transactions completed in Dublin for the last number of quarters. We believe that prime yields in this sector remain stable at approximately 9.5% at the end of Q2.