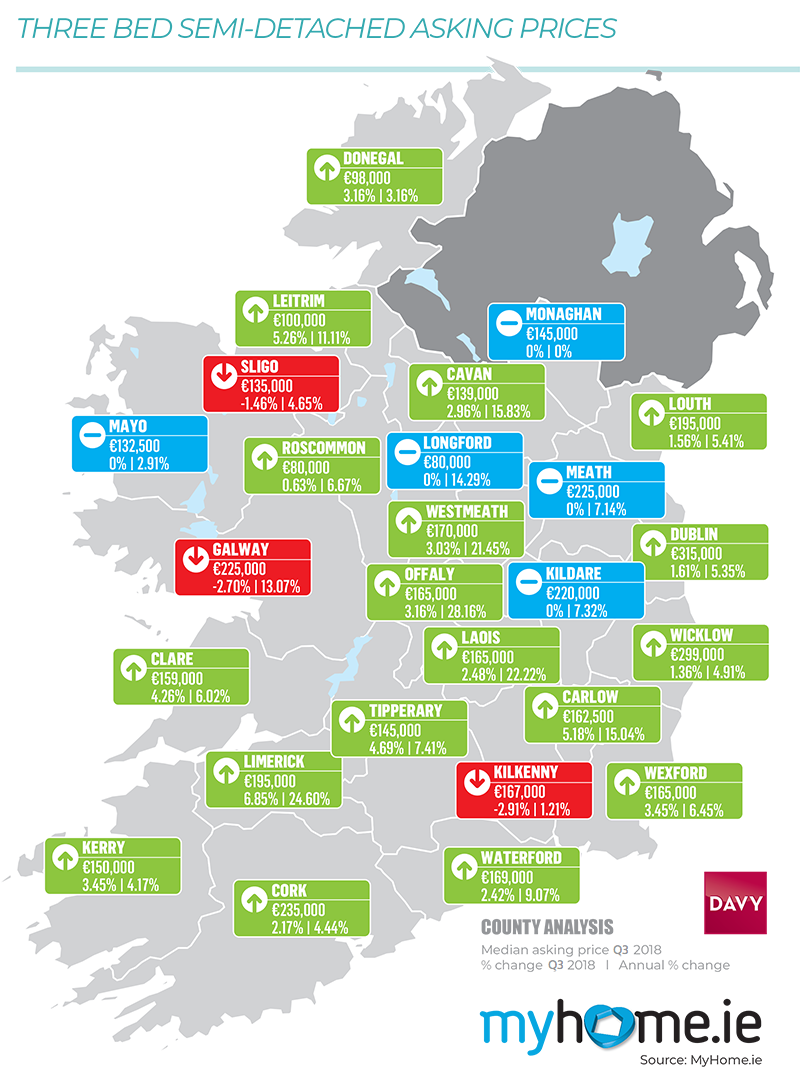

Asking prices fell by 2.5% in Dublin in the third quarter and by a more modest 0.8% nationally, according to the latest residential property price report from MyHome.ie.

According to the report, which is published in association with Davy, the annual rate of inflation for newly listed properties nationally is now 5.9% while it's just 2.2% in Dublin, the slowest pace of increase in two years.

This means the median asking price for new sales nationally is €268K down €2K from the last quarter while the price in Dublin is €375K, down €9K. Newly listed properties are seen as the most reliable indicator of future price movements.

The author of the report, Conall MacCoille, Chief Economist at Davy, said asking price inflation has slowed as expectations for future growth have been reined in.

The double-digit price inflation we experienced earlier this year was simply not sustainable and the slowdown we predicted earlier this year has now materialised. While the magnitude of the drop this quarter may be surprising, some of the quarterly decline may be seasonal, reflecting typically weaker prices at the end of a busy summer trading season.

Some also may be temporary as it was always likely that house price inflation in Dublin would slow following the tightening of the Central Bank mortgage lending rules. These rules were aimed at preventing buyers reacting to stretched affordability by over borrowing, and they have been successful in this regard. Interestingly the MyHome data indicates that the slowdown is still concentrated in the most expensive property types and locations. For example, the median asking price for one-bedroom apartments was up 11% in the year to Q3 2018 to €200K. In contrast median prices for four-bedroom detached homes were flat on the year at €650K.

With jobs and wages growth both exceeding 3%, underlying demand remains exceptionally strong and we expect inflation to equal 8% by December. Brexit of course remains something of a wild card but the key assumption here is that the UK will move to the transition period in March next year, maintaining the status-quo by effectively remaining inside the single market, he said

The report highlighted a pick-up in homebuilding activity. In the 12 months to June 2018 completions equalled 16,300, already well ahead of the 14,446 recorded in 2017. In total planning permissions for 26,750 units have been granted in the 12 months to June.

Angela Keegan, Managing Director of MyHome.ie said the increase in homebuilding was beginning to feed through to improved stock levels, particularly in Dublin.

There were 22,658 residential properties listed for sale on MyHome.ie in September, up 6% on last year. This is the second consecutive quarter in which the stock listed for sale has increased, breaking the downward trend over the past six years. The improvement is even better in Dublin with 5,000 properties listed for sale, up 18% on last year.

We are also seeing an increase in transaction figures. The Property Price Register indicates that 34,706 properties have been sold so far this year and we estimate this represents a 6% growth in transaction volumes, although the register is not yet fully up to date. We believe the total figure of transactions for the year will be close to 60,000, which would be an increase of around 9%.

The average time to sale agreed continues to decline – nationally its 3.5 months, down from 3.8 months previously. In Dublin it's steady at 2.9. This is consistent with higher transaction levels rather than a result of any slowdown in the housing market

Ms Keegan said.