Asking price inflation softens to lowest rate in almost two years

Annual asking price inflation has softened to its lowest rate in almost two years, according to the latest quarterly house price report from MyHome in association with Bank of Ireland.

The last time asking price inflation was lower than the current rate was in Q4 2023, at 4.1%.

This softening in inflation has been driven by increasingly stretched affordability and the process of first-time buyers availing of the Central Bank’s increased borrowing limits having largely played out.

According to the report, a chasm now exists between first-time buyers desperate to secure a property and existing homeowners unwilling to move.

First-time buyers have drawn down 27,000 mortgages over the past year – the highest level since 2007. Meanwhile, the 9,200 mover mortgages drawn down over the same period is close to the lowest level in a decade.

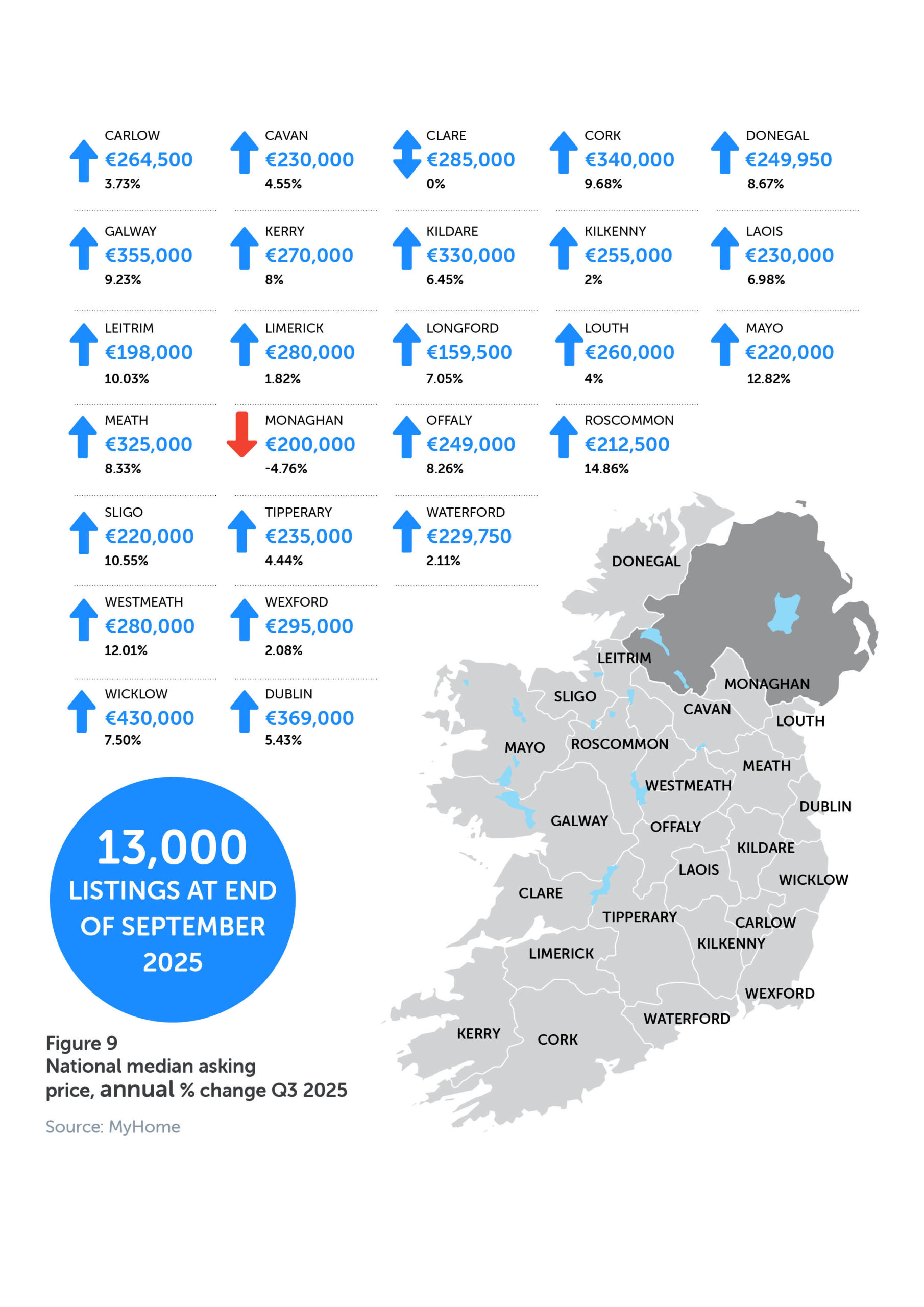

The MyHome report for Q2 2025 found that annual asking price inflation was 5.7% nationwide. Annual asking price inflation in Dublin is now 4.8% and the rate is 6.2% in the rest of Ireland.

Meanwhile, the report found asking prices nationally fell slightly by 0.4% on the quarter, were flat in Dublin and fell by 0.4% in the rest of the country.

This means the median asking price for new instructions nationally was €385,000 in Q3. In Dublin it was €475,000 and in the rest of the country it was €340,000.

Other findings include:

- In September, homes sold for 8% above the original asking price on average, a fresh high.

- There are currently just 13,000 properties listed for sale on MyHome, flat on the year and well down from 20,000-plus level seen prior to the Covid-19 pandemic.

- The average residential property sold in 2025 had a price of €426,000, eight times’ average earnings of €53,000. By this metric Irish house price-to-earnings are now at their most expensive level since 2009.

- Housing completions rose to 32,700 in the twelve months to June, the highest level since the Celtic tiger era.

- Average rents still imply yields of circa 5%, well above current retail mortgage interest rates of 3-4%.

Analysis:

The author of the report, Conall MacCoille, Chief Economist at Bank of Ireland, said: “The MyHome report provides evidence house price inflation is finally slowing down. But the pace of price rises is merely softening. The market is still extremely difficult; there are currently just 13,000 properties listed for sale on MyHome, flat on the year and still down from the levels exceeding 20,000 seen prior to the Covid-19 pandemic.”

Mr MacCoille said that even though affordability was becoming more stretched, competition in the market was still fierce. “The average residential property sold in 2025 had a price of €426,000, eight times the average earnings of €53,000. By this metric Irish house price-to-earnings are now at their most expensive level since 2009.

“However, such is the level of competition among homebuyers that the typical property in September was sold 8% above the original asking price, a fresh high. A fifth of transactions was settled at 20% or more above asking.”

He said that despite the difficult market, home completions represented a silver lining, rising to 32,700 in the twelve months to June, the highest level since the Celtic Tiger era.

“Misleading reports that homebuilding was likely to contract in 2025 have proven well wide of the mark. Encouragingly, the 4-Dublin Housing Supply Pipeline shows there were 22,711 units under construction in the capital in Q1 2025, up 27% on the year. Hence, we are sticking with our forecast for 34,500 completions in 2025.”

Mr MacCoille said it was likely that the sharp pace at which first-time buyers have taken on higher levels of mortgage debt would slow next year and added that it wasn’t too surprising to see the Irish housing market “pause for breath”.

“Two years of ‘high-single-digit’ price gains have stretched affordability. House prices are now likely to rise closer to the current pace of average earnings growth at 5%. This certainly isn’t the solution to Ireland’s housing problem. However, at least the deterioration in affordability seems to be levelling off for now.”

Joanne Geary, Managing Director of MyHome, said: “It is encouraging to observe that home completions have reached their highest level in nearly two decades, suggesting that the Government’s sustained emphasis on supply is yielding positive outcomes. It was also noteworthy to see Budget 2026 introducing measures that will help to boost supply, including a cut in the rate of VAT on completed apartments from 13.5% to 9%.

“Nonetheless, significant improvements in supply are likely to be evident only over the medium to long term, so maintaining momentum remains critical. The Government should continue to seek and implement effective measures to further encourage homebuilding activity.”