Trump’s tariff threat fails to dent ‘fierce’ housing demand

The threat of a pending US-EU tariff war has had a negligible impact on the Irish property market, according to the latest quarterly house price report from MyHome in association with Bank of Ireland.

Strong demand for properties is still a notable feature of the market, with the typical residential transaction being settled for 7.5% above the asking price. This trend has been driven by several factors including significant increases in both the volume and value of mortgage approvals, persistently inadequate supply, and the loosening of mortgage lending rules.

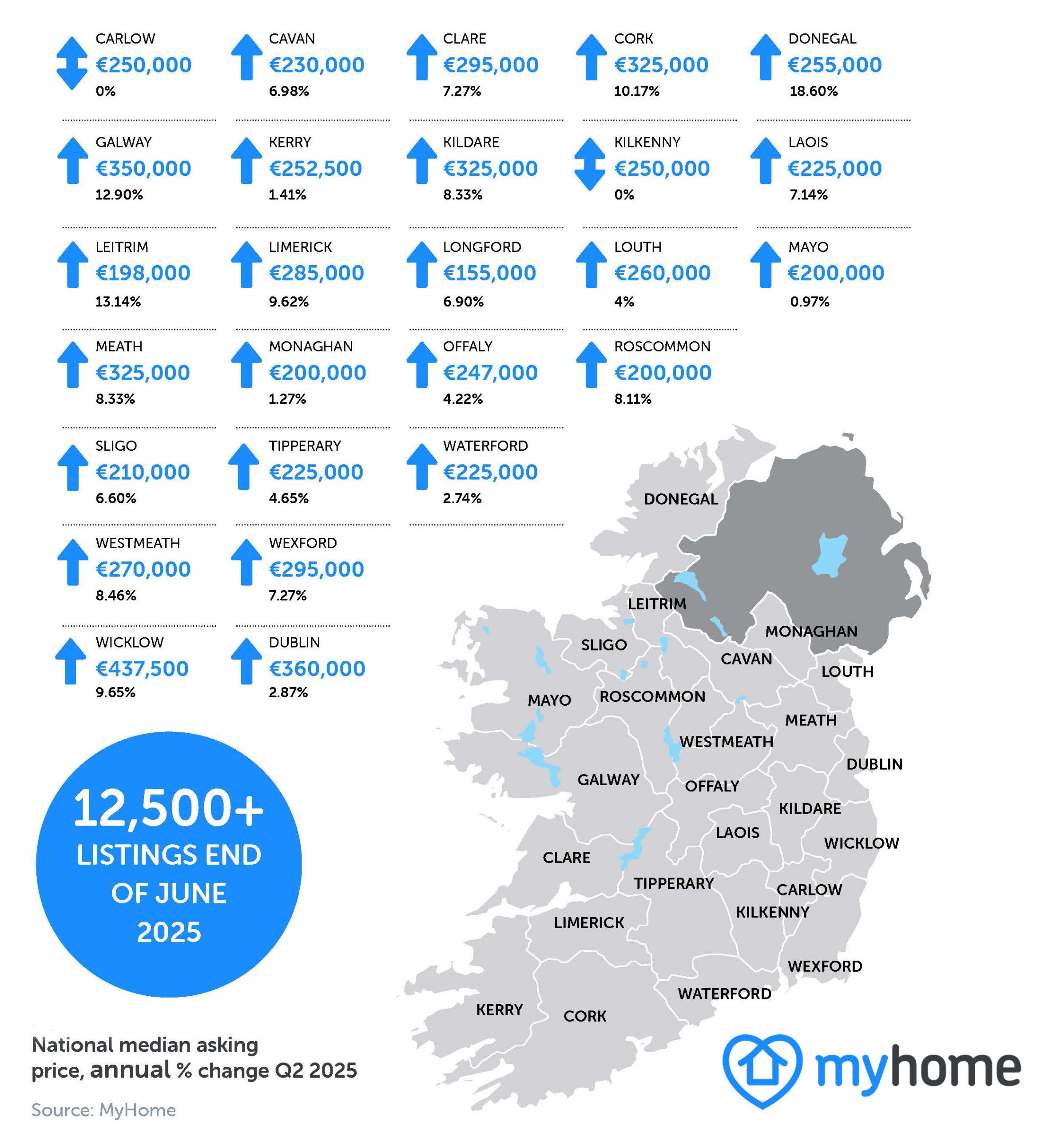

The MyHome report for Q2 2025 found that annual asking price inflation was 7% nationwide. Annual asking price inflation in Dublin is now 5.1% and the rate is 7.9% in the rest of Ireland.

Meanwhile, the report found asking prices nationally rose by 4% on the quarter, by 2.2% in Dublin and by 5.4% in the rest of the country.

This means the median asking price for new instructions nationally was €395,000 in Q2. In Dublin it was €495,000 and in the rest of the country it was €340,000.

Other findings include:

- The average mortgage approval in May was €337,000, up 6.7% on the year, helped by annual pay growth of 5.6% in the Irish economy. There were 43,070 mortgage approvals in the year to May, up 10.5% on 2024.

- At end-June 2025 there were 12,563 properties listed for sale on MyHome, up by just 1% compared with the same period of 2024.

- The average time to sale agreed is now 2.6 months, again close to a historic low and indicative of a very tight market.

- Close to half (47%) of first-time buyers have a mortgage with a loan-to-income (LTI) ratio of 3.5x-4x, up from just 5% two years ago.

- Dublin could see a modest rise in completions in 2025; the ‘4Dublin Housing Supply’ returns indicate that at end-2024 there were 16,260 apartments and 3,185 houses under construction on 188 active sites in the capital, up 24% and 19% respectively on late 2023.

- RTB data indicates average monthly rents were €1,670 at end-2024, up 5.5% on the year – close to the softest pace of rent price inflation in almost four years. Rent reforms will likely mean the pricing gap between new and existing tenancies will be eliminated.

Analysis:

The author of the report, Conall MacCoille, Chief Economist at Bank of Ireland, said: “Uncertainty following President Trump’s announcement of ‘Liberation Day’ tariffs hasn’t been sufficient to dent Ireland’s housing market. The average mortgage approval in May was up 6.7% on the year, while the typical residential transaction is being settled 7.5% above the original asking price. Meanwhile, one in six properties is sold by 20% or more over asking price, indicating that competition for homes remains fierce.

“Another factor at play is loosening of the Central Bank mortgage lending rules. The average first-time-buyer borrowed 3.4 times’ their income in 2024, up from a 3.2x multiple in 2022. This change has pushed up house prices by €15,000 to €20,000.”

Mr MacCoille added: “That said, the process of rising leverage may be coming to an end. The proportion of first-time buyers taking out a mortgage with a 3.5-4x loan-to-income (LTI) multiple is now steady, at just under 50%. If so, Irish house price inflation is more likely to return to mid-single digit territory.”

He said that some improvement in home completions was likely in 2025. “The ‘4Dublin Housing Supply Pipeline’ figures, the only survey of current homebuilding activity, shows the number of houses under construction in Dublin at end-2024 up 19% on the year.”

However, he warned that: “Whatever the outcome for housing completions in 2025, it will fall well short of the 50-60,000 units required. Attention should focus on difficult problems surrounding build costs and the viability of apartment development in Ireland over the medium-term.”

He said that newly introduced rent controls would likely serve to eliminate the two-tier rental market, as RTB figures from end-2024 show new tenants were paying on average €240 per month in rent more than those in existing tenancies.

Joanne Geary, Managing Director of MyHome, said: “The volatile geo-political climate in which we are living is particularly unhelpful for the economy. It is promising that, to date, the threat of US-EU tariffs does not appear to have had a major negative effect on the market, but it remains to be seen what the coming months will bring.

“As ever, we need to focus on what we can actually control, which means continuing efforts to significantly increase our national stock of properties, and urban apartments in particular.”