The Q4 2022 report, in association with Davy, found that annual asking price inflation slowed to 6% nationwide, and was 3.6% in Dublin and 7.6% elsewhere around the country.

Meanwhile, the report found quarterly asking price inflation dropped by 0.4% nationally, by 0.8% in Dublin, and by 0.2% elsewhere around the country.

This means the median asking price for new instructions nationally is now €330,000, while the price in Dublin is €436,000 and elsewhere around the country it is €283,000.

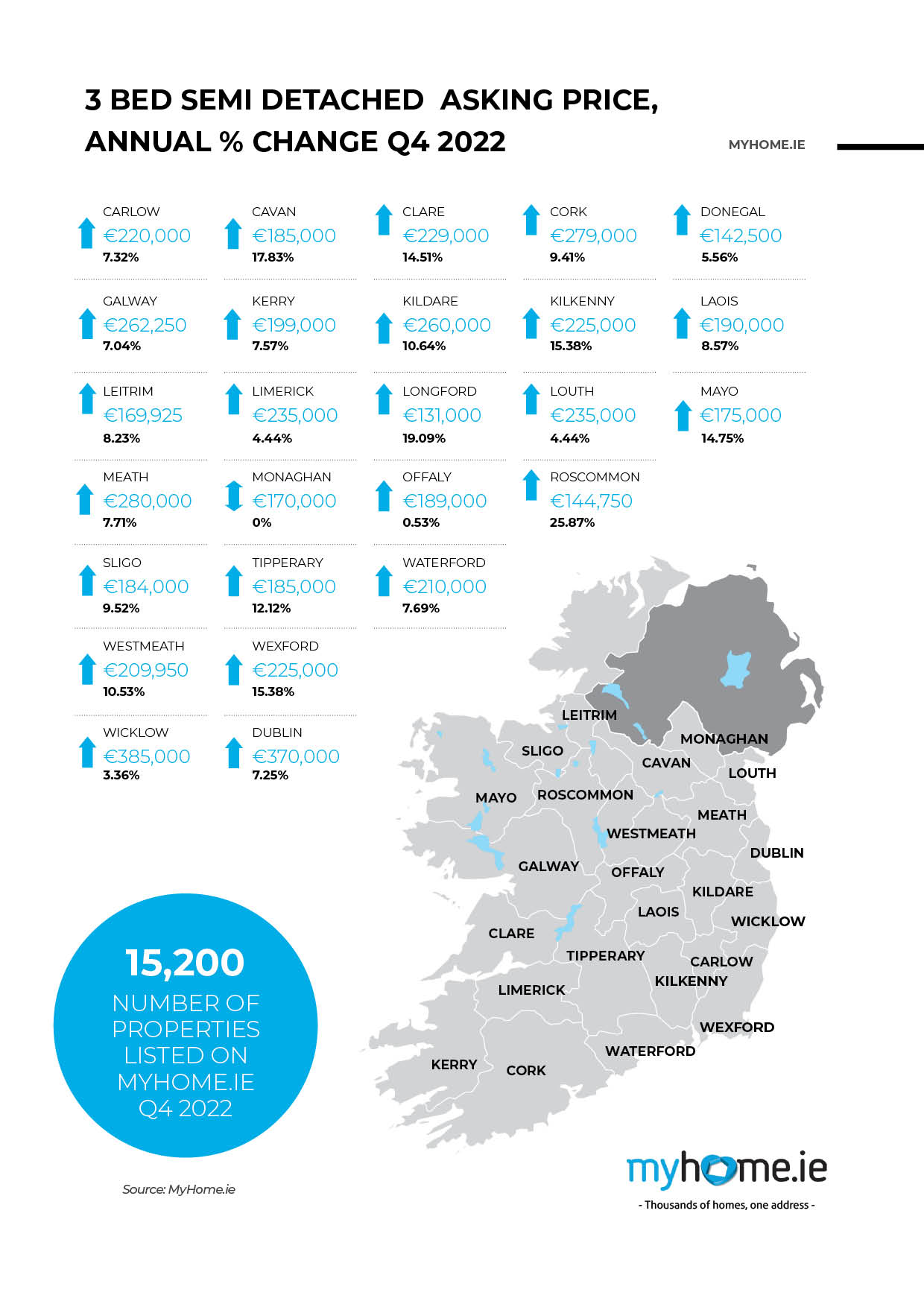

• There were 15,000 available properties for sale on MyHome.ie in Q4 – an improvement on the same time last year but still below pre-pandemic levels.

• Average time to sale agreed in Q4 was 2.7 months nationwide which is indicative of a very tight housing market.

• Average mortgage approval in October was €280,600 – up 4.3% on the year.

• Residential property market transactions are set to exceed €21bn in 2022 – up 7.5% in volume terms on 2021.

• The average residential transaction in Q3 2022 was €370,000, now 7.7x the average income of €48,000 which is the highest multiple in over a decade.

• We expect to see 28,400 housing completions in 2022 – which would exceed our previous forecast of 26,500 units completed.

• The CSO estimates that private rents rose by 11% to the year in November. Gross rental yields of 5-6% are still higher than average mortgages rates of less than 3% which suggests that, for those who can get on the ladder, there is an incentive to buy over renting.

The author of the report, Conall MacCoille, Chief Economist at Davy, said that it appeared the market had held up better than anecdotal evidence had suggested in 2022. “The number of vendors cutting their asking prices is still at low levels. Also, transactions in Q4 were still being settled above asking prices, indicative of a tight market.

“There are 15,000 properties listed for sale on MyHome.ie, an improvement from the beginning of 2022 but below pre-pandemic levels exceeding 20,000. The average time to sale agreed in Q4 was just 2.7 months, still close to historic lows. We expect transactions will exceed €21bn in 2022, up 7.5% in volume terms on 2021.”

He added that even if mortgage interest rates rise to 4%, debt service ratios are unlikely to become stretched and there will be only a limited headwind to house prices.

But he warned that buyers were stretched to a degree not seen since 2009. “The average residential transaction in Q3 2022 was €370,000, now 7.7x the average income of €48,000. This is a similar valuation multiple to the UK, where house prices are now falling due to a surge in mortgage rates above 6%.”

Mr MacCoille noted that already stretched valuations in Ireland could be exacerbated by the Central Bank’s decision to ease mortgage lending rules to four times’ income. He said this gave an upside risk to the 4% house price inflation prediction for next year.

He added that recent months had seen worrying trends in the homebuilding sector, with housing starts slowing, and the construction PMI survey pointing to the flow of new development drying up.

“We still expect housing completions will pick up to 28,400 in 2022 and 27,000 in 2023. However, the outlook for 2024 is far more uncertain. The government’s ambitious plans to expedite planning processes are welcome although, as ever, the proof will be in the pudding.”

Joanne Geary, Managing Director of MyHome.ie, said that vendor sentiment had been somewhat affected by rising costs and interest rates. “Over 3% of all properties on MyHome.ie saw asking price reductions in Q4, a low rate but even still the highest figure since Q3 2020. However, asking prices tend to fall toward the end of the year; for example, declining by 1.1% on average in the last quarter pre-pandemic. While asking price increases have cooled, the market has still remained remarkably resilient despite the uncertain environment.”

She said that stock levels were still a cause for concern. “Stock levels are improving but are still not running at the levels we need to see in order to satisfy demand. As such, we hope to see inflationary pressures ease in the construction sector over the coming months.”

Full details of the report can be found at www.myhome.ie/reports

#MyHomeDavy