Asking price inflation accelerates despite rising interest rates

The property market is generating momentum, with asking price inflation accelerating despite further interest rate hikes, according to the latest quarterly house price report from MyHome.ie.

The Q3 2023 report, in association with Davy, found that annual asking price inflation was 4.1% nationwide, 3% in Dublin and 4.9% elsewhere around the country.

Meanwhile, the report found asking prices rose marginally by 0.6% on the quarter nationally and by 1.3% in Dublin. Prices rose by 0.4% elsewhere around the country.

This means the median asking price for new instructions nationally is now €330,000, while the price in Dublin is €425,000 and elsewhere around the country it is €285,000.

Other findings include:

- Homes are now being sold for 3% over asking prices, versus 1% at the start of the year.

- The average mortgage approval for first-time buyers hit a fresh record high in July of €298,800, up 4% on the year.

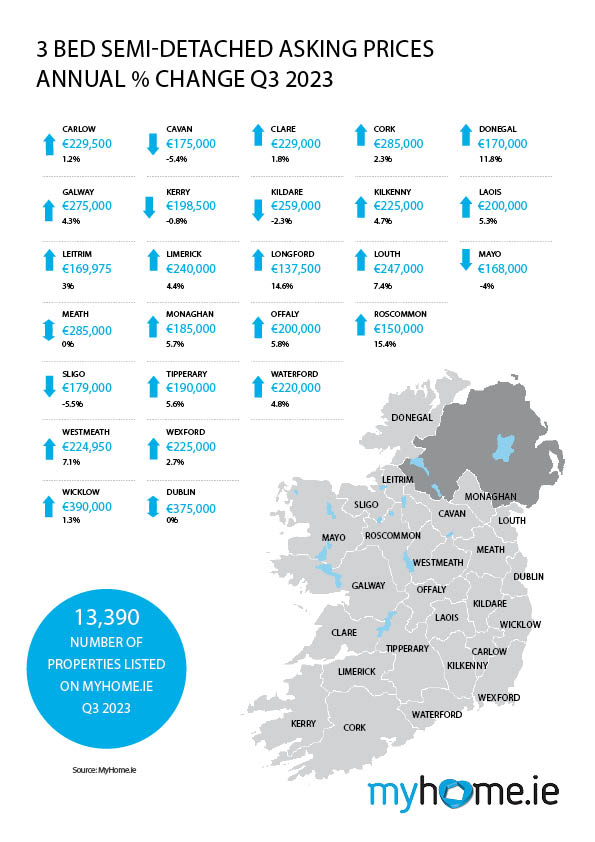

- There were 13,400 available properties for sale on MyHome.ie in Q3 – still well below the pre-pandemic figure of 20,000-plus. This equates to just 0.6% of the 2.1 million total homes in Ireland.

- There were 7,675 new listings on MyHome.ie in Q3 – down a staggering 38% on the year.

- There were 28,900 housing starts in the year to July – but 40,000-50,000 units are needed annually to address our pent-up demand.

- Average rents on new tenancies rose by 2.5% in Q1 2023, up 8.9% on the year to €1,544.

- Tight supply is leading to negative societal consequences, with latest CSO figures showing:

- Ireland’s housing stock per capita is now the lowest across a range of European countries

- Adults living at home with their parents now comprise over 10% of the population

- Numbers of employed adults living at home with parents and adults living with unrelated persons have grown hugely since 2016 (by 28% and 29%, respectively)

Analysis: The author of the report, Conall MacCoille, Chief Economist at Davy, said: “The period of falling house prices we saw earlier in the year has come to an end, with the underlying imbalance between demand and supply providing fresh impetus to the market.”

He said that housing demand had remained resilient, despite interest rate hikes. “That competition for homes is heating up is evident in the 3% premium over the asking price that buyers were prepared to pay in September, up from 1% at the beginning of the year. Furthermore, in July the average mortgage approval was €298,800, up 4% on the year, lending volumes up 18% on 2022.”

He said Ireland had avoided the house price declines seen in the UK and other countries for two reasons. “First off, the Irish economy has performed far better with employment already 12% above pre-pandemic level, an extraordinary pace of job creation. Hence, housing demand has remained robust. Second, the Irish housing market has been less liquid than other countries, so less vulnerable to the unexpected rise in ECB rates.

However, he noted that supply was still a major issue. “The figures suggest any period of catch-up for housing activity following the Covid19 pandemic is now over. Worryingly, homebuyers may have to reconcile themselves to this tighter market.”

Mr MacCoille added that while we saw 28,900 housing starts in the year to July, we needed 40,000-50,000 units annually to address our pent-up demand.

He said that, while affordability was stretched and the impact of past ECB interest rate hikes had yet to be fully felt, the surprise loosening of the Central Bank mortgage lending rules earlier this year would add fuel to house prices over time.

“We expect modest, low single-digit price rises from here, close to the pace of pay growth, so affordability is stable or improves marginally. However, this quarter’s MyHome report highlights the risk that the lack of housing supply could drive more aggressive price gains over the next one to two years.”

Joanne Geary, Managing Director of MyHome.ie, said that our ever-present problems with supply were concerning. “We know that there were just 13,400 homes listed for sale on MyHome.ie at the end of the third quarter, which is down from the pre-Covid figure of 20,000-plus. Even more striking is the marked decline in new listings on the website; there were just over 7,500 new listings during Q3, down a massive 38% compared with the same period last year.”

She said this lack of stock has had inevitably negative societal consequences. “Recent CSO data shows us that the cohort of employed adults living with their parents has grown by 28% since 2016. Similarly, the average household size for those adults living with unrelated persons was now 3.72. This is unsustainable and will rightly be front of mind for the Government as it considers Budget 2024 next week.”