The Q3 2022 report, in association with Davy, found that annual asking price inflation slowed to 7.8% nationwide, and was 6.2% in Dublin and 9% elsewhere around the country.

Meanwhile, the report found quarterly asking price inflation dropped by 1.3% nationally, by 1.1% in Dublin, and by 1% elsewhere around the country.

This means the median asking price for new instructions nationally is now €320,000, while the price in Dublin is €420,000 and elsewhere around the country it is €275,000.

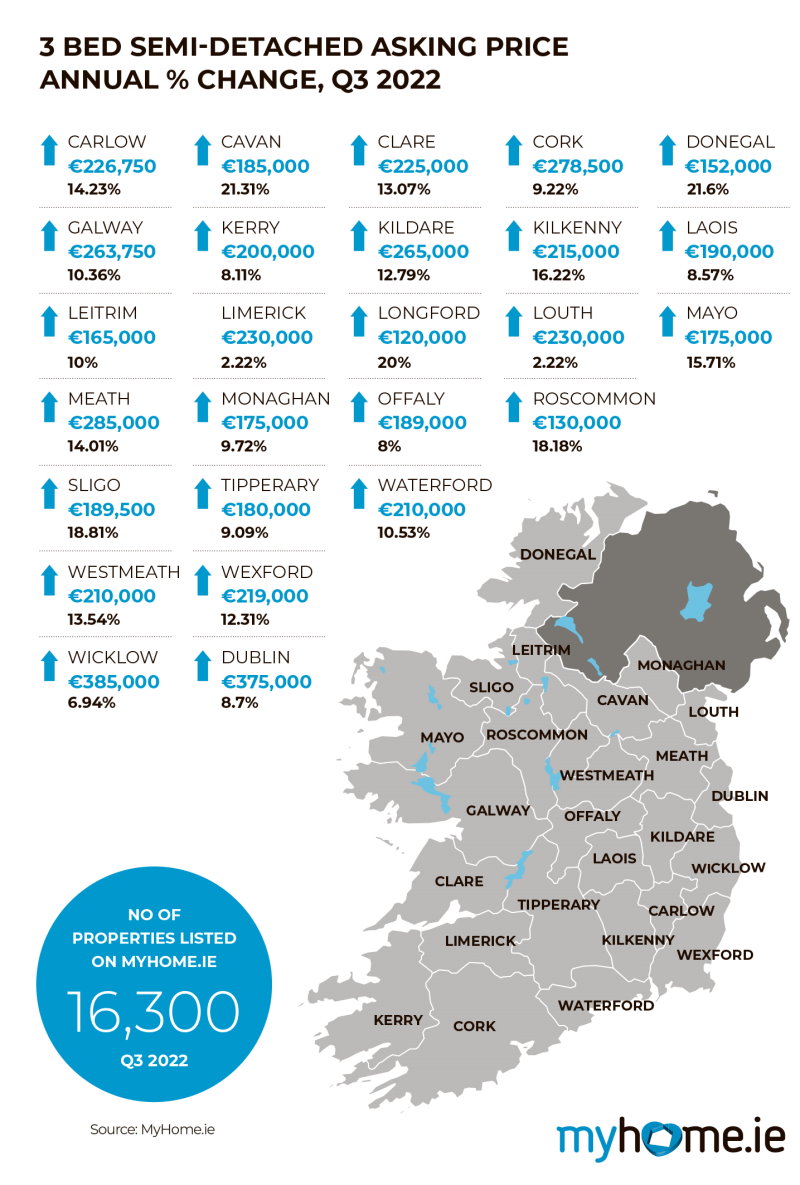

• Continued evidence of vendors returning to the market with the number of available properties for sale on MyHome.ie rising to 16,300 in September 2022 – an increase of 46% compared to the start of the year.

• Average time to sale agreed in Q3 fell to 2.6 months nationwide which is indicative of a very tight housing market.

• Average mortgage approval rose to €288,300 – up 8% on the year.

• Residential property market transactions in the first eight months of 2022 are up 8.1% on 2021 and 6.8% on 2019.

• Over 7,600 housing units were completed in Q2 – the calendar year total for 2022 now looks set to exceed our previous forecast of 26,500 units completed.

The author of the report, Conall MacCoille, Chief Economist at Davy, said that the latest figures did not necessarily mean we would see persistent price falls. “Asking prices are typically weak as the busy summer trading season peters out and fell in both Q3 2018 and Q3 2019. After the disruption of the Covid-19 pandemic, the usual seasonal pattern has re-emerged.”

He said that there was mixed news on supply. “On one hand, new listings for sale are strong, suggesting the market is merely making up for lost time following delayed transactional activity in 2020 and 2021. However, it is most unwelcome to see construction activity curtailed by supply chain issues and rising input costs.”

He said rising interest rates will lead to slower price growth, but that pent-up demand in the market remained strong. “In July, the average mortgage approval was €288,300 – up 8% on the year. In the year to June, 16% of mortgage approvals failed to translate into a drawdown, indicative of frustrated buyers. Similarly, the 30,000 applications to avail of the Help-to-Buy scheme over the past 12 months are well in excess of claims of just 7,400. Plus, more than 1,000 applications have been lodged for the government’s First Home Scheme since it opened in July.”

He said that price growth would continue, albeit at a slower rate. “Looking forward, we expect that Irish house asking prices will grow by 6% through 2022 and by 3% in 2023. There are of course many risks to this view. Ireland potentially faces an energy crisis this winter amid fears of a full-blown European recession brought on by events in Ukraine and surging natural gas prices.”

Joanne Geary, Managing Director of MyHome.ie, said: “It appears that a number of factors have eased the runaway asking price inflation we were seeing earlier this year. This is in line with our predictions throughout the year and it is important to note that this represents a much-needed correction in the market.”

She noted that rising stock levels were a cause for optimism. “One promising sign for would-be homebuyers this quarter is increasing supply, albeit from a low base. New listings on MyHome.ie are up 33% year on year, while there has been a 25% increase in the amount of properties featured on the website since last year. This supply is badly needed, as demand is still particularly strong. On MyHome.ie, leads are up by 27% and brochure views are up 15% compared to this time last year.”

In addition, she noted that Budget 2023 could have done more for the rental market. “The supports announced for renters are welcome, but these should have been accompanied by significant supports for small landlords to encourage them to stay in the market. The failure to adequately address the predominant issue of lack of supply by supporting small landlords to stay in the market is a missed opportunity.”

Full details of the report can be found at www.myhome.ie/reports

#MyHomeDavy