Strong labour market and looser lending rules driving prices skyward

The sustained strength of the Irish labour market, along with the impact of looser mortgage lending rules and the continual poor supply of properties, has driven annual asking prices to their highest level in almost two years and will likely lead to a gain of 5-6% over the year in full, according to the latest quarterly house price report from MyHome.ie in association with Bank of Ireland.

The Q2 2024 report found that annual asking price inflation was 7.3% nationwide. The last time this annual figure was higher was in Q3 2022, when inflation was 7.8% nationwide.

Annual asking price inflation in Dublin has now accelerated to 7.2%, and to 7.6% in the rest of Ireland.

Meanwhile, the report found asking prices rose by 5.1% on the quarter nationally, by 3.3% in Dublin and by 6.7% outside the capital.

This means the median asking price for new instructions nationally in Q4 was €365,000. In Dublin it was €465,000 and elsewhere around the country it was €310,000.

Other findings include:

- A 4.7% rise in average earnings to €50,300 in the year to Q1 2024 has had an impact, with a 4.6% rise in average mortgage approval values to €313,000 recorded in the year to April.

- The loosening of the Central Bank mortgage lending rules has seen the share of first-time buyers with a loan-to-income ratio on their mortgage between 3.5x-4x leap from 6% in 2022 to 36% last year

- In May, houses were being sold for 6% over the original asking price, at the median. This is a stark change to 2023, when the median premium was just 1%.

- The average time to sale agreed nationwide was just over 11 weeks in Q2 2024, which is close to a record low.

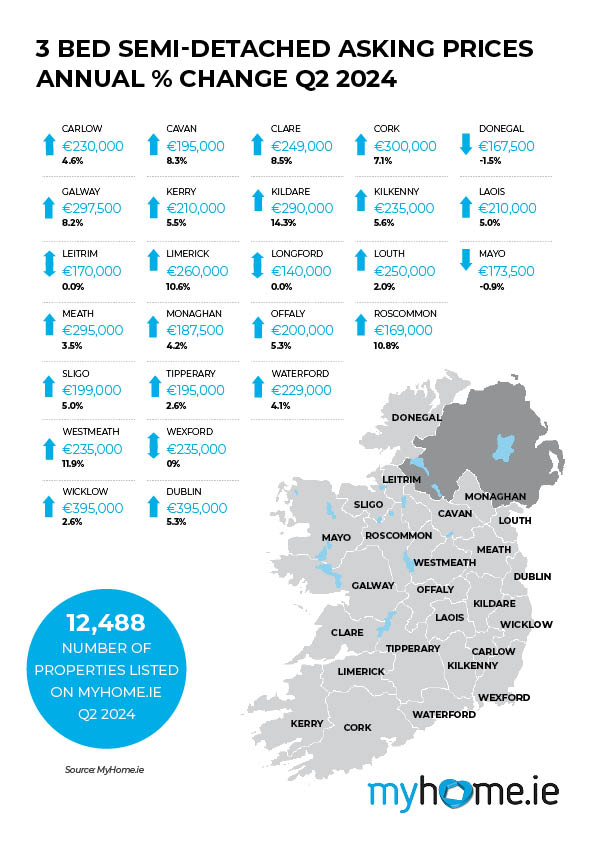

- The number of properties listed for sale on MyHome.ie was just 12,500 at end-June, still close to the historic low in Q1 2024 and down 11% on 2023.

- However, homebuilding activity is positive. There were 32,121 housing starts in the first five months of 2024.

- The rate of rent inflation softened to 4.9% in May.

Analysis:

The author of the report, Conall MacCoille, Chief Economist at Bank of Ireland, said: “The clear message from the Q2 2024 MyHome.ie Property Price Report is that house prices have gained further momentum. Asking prices rose by 5% in Q2 2024, up 7.3% on the year, the highest figure since Q3 2022.

“This represents an acceleration in the pace of annual asking price inflation from 6.5% in Q1 2024. Furthermore, the pick-up in the pace of asking price inflation has been broad based across Dublin (7.2%) and the rest of Ireland (7.6%).”

He said that the sustained strength of the Irish labour market was having a significant effect. “The 4.7% rise in average earnings to €50,300 in the year to Q1 2024 was always likely to push up house prices. Indeed, the average mortgage approval in April was €313,000, also up 4.6% on the year.” He added that the relaxation of the Central Bank mortgage lending rules for first-time buyers had seen the share of first-time buyers with a loan-to-income ratio on their mortgage between 3.5x-4x leap from 6% in 2022 to 36% last year.

“The fierce competition between homebuyers has continued into the second quarter, with residential transactions in May being settled by 6% on average above the original asking price,” he said.

Another factor impacting prices is the continual poor levels of property supply in the market. “There were just 12,500 properties listed for sale at end-June, still close to the historic low in Q1 2024 and down 11% on 2023. To some extent this appears to reflect a hangover from 2023, when reports of falling house prices, stretched affordability and ECB rates led many would-be vendors to incorrectly fear demand was soft. This trend may reverse but will take time,” Mr MacCoille said.

“The second quarter of the calendar year is particularly important for asking prices, set ahead of the busy summer trading season, before the market cools heading into the winter. The momentum in the market means a high single digit gain in the order of 5-6% for the year in full now looks likely.”

Joanne Geary, Managing Director of MyHome.ie, said: “The strength of our labour market is of course a positive thing, but without an adequate supply of properties to meet the demand generated by rising incomes, it is inevitable that competition will remain intense. It will take time for the growing rate of housing starts to have a real impact, but it is promising to see this figure move in the right direction.”